The $5 Trillion Milestone Everyone Missed

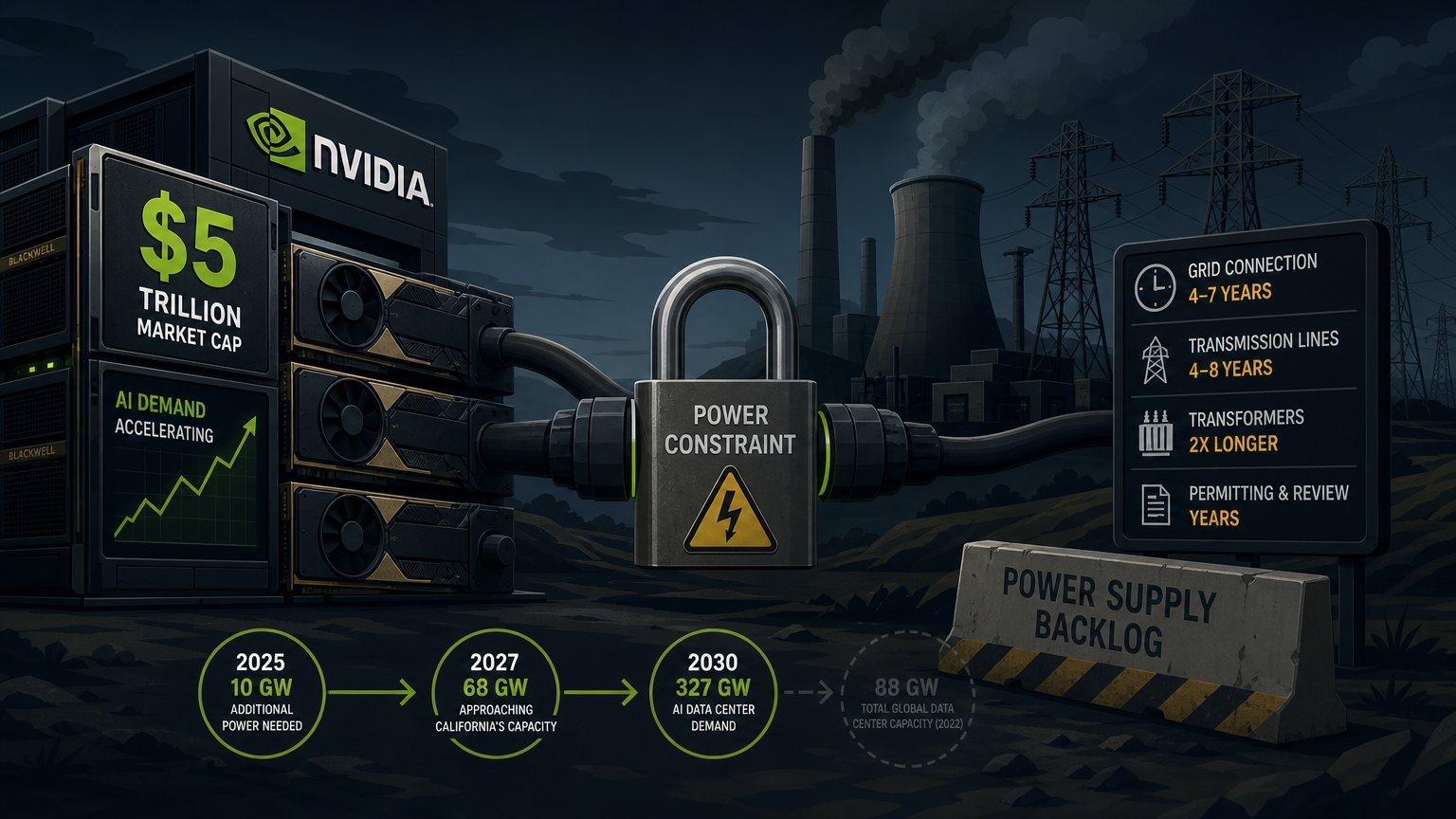

On October 29, 2025, Nvidia made history by becoming the first company to reach a $5 trillion market capitalization. The stock closed more than 3% higher, capping a meteoric rise that saw the company grow from $4 trillion just three months earlier. CEO Jensen Huang disclosed that Nvidia has secured more than $500 billion in orders for its AI chips through the end of 2026, with plans to ship 14 million Blackwell units over the next five quarters.

The Blackwell architecture is impressive by any measure: 208 billion transistors (2.5x the previous generation), delivering up to 20 petaFLOPS of FP4 AI compute. The tech press celebrated. Wall Street cheered. Everyone assumed the hard part was over—if you could get your hands on the chips, you could build AI infrastructure at scale.

They were wrong.

The Question That Changed My Perspective

Two weeks ago, a vendor contacted our team with what seemed like a straightforward request: "Do you have access to 20 megawatts of power for our deployment?"

Twenty megawatts. For context, that's enough electricity to power roughly 15,000 homes continuously. They weren't asking if we could arrange it eventually, or if we knew someone who might have connections. They were asking if we had it available, as if 20 MW of power capacity might just be sitting around waiting for someone to claim it.

The answer, of course, was no. But the question itself revealed something more troubling: in the AI infrastructure world, requests like this are becoming routine. And they're rarely being fulfilled.

The Numbers Don't Add Up

Here's what the data tells us: globally, AI data centers will need an additional 10 gigawatts (GW) of power capacity in 2025 alone—more than the entire state of Utah's power capacity. By 2027, that number jumps to 68 GW, approaching California's total power capacity. By 2030, we're looking at 327 GW of AI data center demand, compared to just 88 GW of total global data center capacity in 2022.

Let that sink in: in eight years, AI alone will require nearly four times what all data centers combined used just three years ago.

The math gets worse when you look at individual deployments. Ten years ago, a 30 MW data center was considered large. Today, 200 MW is normal, and some facilities are approaching 1 GW—a gigawatt!—in capacity. Training a single large language model like GPT-4 required approximately 30 MW of continuous power. Nvidia's latest DGX H100 servers consume about 10,200 watts each, and their next-generation GB200 systems with their servers may require rack densities of up to 120 kilowatts per rack.

The Infrastructure Gap: Why Power Is Harder Than Chips

Nvidia can scale chip production. TSMC can build new fabs. But you can't manufacture electricity, and you can't download it from the cloud. Power infrastructure operates on decade-long timelines that clash violently with the AI industry's quarterly planning cycles.

Consider the barriers:

Grid Connection Wait Times: Four to seven years in key regions like Virginia. Some projects are facing connection requests that won't be fulfilled until 2030 or later.

Transmission Infrastructure: Building new transmission lines takes four to eight years in advanced economies. Wait times for critical grid components like transformers have doubled in the past three years.

Generation Capacity: Even if you have grid access, where does the power come from? Many utilities are warning they "don't have the electrical infrastructure to meet the aggressive targets" AI companies are announcing.

Regulatory Constraints: Environmental reviews, local opposition, and permitting processes can add years to any power infrastructure project.

According to analysts, unless these risks are addressed, around 20% of planned data center projects could face significant delays—and those are just the projects that were realistic enough to get planned in the first place.

Real-World Impact: What This Means for Your AI Strategy

If you're a technology leader planning AI deployments, here's what the power crisis means in practical terms:

1. Location Constraints Trump Everything

You can't build where you want to build. You can build where power exists. This is forcing a fundamental rethinking of data center strategy. Some regions that seemed ideal for other reasons—proximity to markets, existing infrastructure, tax incentives—become non-starters simply because the grid can't support the load.

I've watched deployment timelines slip not because of chip shortages or engineering challenges, but because the power just isn't available. Teams that assumed they could secure capacity in 6-12 months are finding 3-5 year timelines more realistic.

2. Power Is the New Real Estate

Remember when location, location, location was about land? In AI infrastructure, it's about megawatts. Organizations are now evaluating regions primarily based on available electrical capacity, with other factors becoming secondary considerations.

This is creating surprising winners and losers among regions competing for AI infrastructure investment. Areas with robust power grids and progressive utility policies are seeing unprecedented demand, while historically tech-friendly locations without adequate power infrastructure are being passed over.

3. The Cloud Providers Are Struggling Too

Don't assume this is someone else's problem that you can solve by going cloud-native. AWS, Google Cloud, and Microsoft Azure are facing the same constraints. When hyperscalers can't get power allocation for new regions, their growth plans stall just like everyone else's.

The cloud providers have advantages—existing relationships, massive scale, long-term planning—but they're not immune. Some are reportedly paying premiums for power capacity or making strategic decisions about which regions to prioritize based primarily on power availability.

4. Cost Structures Are Changing

The vendor who asked for 20 MW wasn't just asking if we had it—they were implicitly asking what it would cost. Power pricing for AI workloads is becoming as important as compute pricing. In some markets, electricity costs are becoming the dominant factor in total cost of ownership, exceeding even the amortization of expensive GPU hardware.

Organizations accustomed to thinking about compute efficiency in terms of FLOPs per dollar now need to think in terms of FLOPs per kilowatt-hour. The vendors who master power efficiency will have sustainable competitive advantages.

What You Can Do Now

Despite the grim outlook, there are practical steps technology leaders can take:

Short-Term: Optimize What You Have

- Measure Everything: If you're not tracking power consumption at the rack level, start now. You can't optimize what you don't measure.

- Workload Scheduling: Not all AI workloads need to run 24/7. Some training jobs can be scheduled during off-peak hours or moved to locations with better power availability.

- Model Efficiency: The conversation about model compression, quantization, and distillation isn't just academic—it's economic. Smaller, more efficient models require less power.

- Hardware Selection: When evaluating GPUs, watts per FLOP matters as much as raw performance. The fastest chip isn't always the most strategic choice.

Medium-Term: Strategic Planning

- Multi-Region Strategy: Don't assume your preferred location will have power available when you need it. Develop relationships and optionality in multiple regions.

- Power Partnerships: Start conversations with utilities now, not when you need capacity. Some organizations are getting creative—co-developing generation capacity, investing in local grid improvements, or partnering with existing power-intensive industries.

- Hybrid Architecture: Design systems that can distribute workloads across multiple sites based on power availability, not just performance requirements.

Long-Term: Infrastructure Investment

- On-Site Generation: Some organizations are exploring on-site power generation—not as a primary strategy, but as a hedge against grid uncertainty. Natural gas, solar with battery storage, and even small modular nuclear reactors are in the conversation.

- Efficiency Innovation: The companies that will win are those that can deliver the same AI capabilities with 50% of the power. This isn't just about hardware—it's about algorithms, architectures, and system design.

The Uncomfortable Truth

Nvidia's $5 trillion valuation reflects real demand and real technological achievement. But it also represents a bet that the infrastructure to actually use all those chips will materialize. That's not a given.

We're at a point where the technology industry's ambitions have outpaced physical infrastructure in a way we haven't seen since the early days of the internet, when bandwidth constraints limited what was possible regardless of what software could theoretically do.

The difference is that power infrastructure operates on longer timelines and faces greater physical constraints than laying fiber ever did. You can't disrupt the physics of the electrical grid with a clever startup. You can't download a megawatt.

A Call for Realism

When that vendor asked if we had access to 20 megawatts, they weren't being unreasonable given their needs. They were simply operating in a world where asking for enough power to run a small city has become a normal part of AI infrastructure planning.

The uncomfortable reality is that many AI deployment plans—including those from well-funded organizations with sophisticated engineering teams—are effectively fiction until the power question is answered. Not the chip question. Not the software question. The power question.

As an industry, we need to have honest conversations about timelines, constraints, and trade-offs. We need to invest not just in more efficient AI models, but in more efficient data centers and more strategic relationships with power infrastructure. And we need to make peace with the fact that some ambitious plans will need to be delayed, relocated, or fundamentally redesigned because the power simply isn't there.

Nvidia's $5 trillion milestone is real. The $500 billion in chip orders is real. The technological capabilities are real. But without the megawatts to power it all, it might remain largely unrealized potential—at least on the timelines everyone is promising.

The good news? The organizations that recognize this constraint now and plan accordingly will have substantial competitive advantages. While competitors scramble for power allocation in 2027, the strategic planners of 2025 will already be running production workloads.

The race isn't just for the best chips anymore. It's for the megawatts to run them.

Key Takeaways

- Power, not chips, is the primary bottleneck for AI infrastructure scaling in 2025-2030

- Grid connection timelines of 4-7 years make long-term planning essential

- Location strategy must prioritize power availability over traditional factors

- Cloud providers face the same constraints, so "someone else's problem" isn't a strategy

- Power efficiency is becoming as important as computational efficiency for competitive advantage

- Early action on power partnerships can provide years of competitive lead time

References

- Nvidia Corporation. NVIDIA Newsroom - Financial Results and Announcements

- McKinsey & Company. (2025). AI power: Expanding data center capacity to meet growing demand

- International Energy Agency (IEA). (2025). Energy and AI Report

- RAND Corporation. Pilz, K. F., Mahmood, Y., & Heim, L. (2025). AI's Power Requirements Under Exponential Growth

- U.S. Congressional Research Service. (2025). Data Centers and Their Energy Consumption